Forbidden Arbitrage

Three amazing trades that you shouldn’t make.

Tomorrow, I start my job as a trader at Jane Street. Soon after that, I will register as a financial professional, a title that subjects me to FINRA scrutiny and a host of rules governing the things I buy, the work I do, and the words I say. For good reason: you demand probity from the people handling your money and investments. All this financial machinery is duct-taped together by popular faith in institutions and regulations, and as the SBF incident demonstrates, stripping the adhesive sends the whole thing tumbling. No good. So, unlike my predecessor, Sam, when I walk into the office tomorrow, I’m leaving my fraud blueprints in the lobby.

And by lobby, I mean this blog. Here are my most lucrative, legally-dubious, FINRA-infuriating arbitrage ideas—keys to either the penthouse or the penitentiary. If you know why they wouldn’t work, share with the class in the comments. If you for some reason choose to try, tell me so I can stop you. Nota bene: not financial advice.

Evasion Edge

The IRS lets you write off gambling losses. If you win some money on slots and lose it all on blackjack, the loss cancels the gain and you don’t have to pay any tax. It has to be this way or else gambling would burn money faster than you could enjoy the flames.1 Of course, gambling losses are considered “other income,” so you can’t just write off losses against your earned income.

Unless gambling is your income source. If you’re a professional gambler, then your evening at the card lounge turns from a “serious problem” to an “operating expense.” You and your friend could spin up an LLC and do the “business” of recording and posting gambling videos.2 Voila! Now, when you gamble, you only lose to the house.

Here’s what’s bugging me though. Casinos can only go so far in making you report wins. Specifically, they report 10k+ cashouts and wins above various thresholds between $1200 and $5000. So you and your friend could sit down at the opposite ends of a single-zero roulette table in Vegas. You each bet $4000 on opposite colors. One of you, probably, wins. The winner stuffs the cash in their pocket and goes home. The loser writes off their loss. By my math, you make about 10% return on each bet.3 There are refinements to be made, for sure, but it certainly seems like a degenerate gambler and his buddy could self-fund their Vegas trip on the backs of the IRS.4 I sure hope the IRS does something about this!

Not financial advice.

Alpha: 10% return per tax season, up to $4000

The Deficient Frontier

No risk, no return. A basic premise of investing is that your return—how much you make on average—trades off with your risk—how big of a swing you’re willing to tolerate. The more safe an asset is, the less money you can expect to make from it. Thousands of portfolio managers toil to optimally trade off risk and return, but we’ve known the basics for half a century: there is a theoretical limit to how much return you can get for a given level of risk, and it’s called the efficient frontier.5 Investing is basically about pushing this frontier outward, towards less risk and greater returns. Hedge funds accomplish this by finding uncorrelated returns, letting portfolio managers reduce their overall risk. We need them to do this because, as reasonable human beings, we are risk averse.

And then there’s gambling.

The dotted line is the efficient frontier. Numbers are illustrative.

Like, what the fuck? Participants of this corner of the market actively demand risk. And a lot of it too! U.S. casinos make $65 billion a year in revenue. Online gambling generates $25 billion. One site alone—Stake—makes $2.5 billion a year. And so a tremendous amount of money is poured each year into buying risk.

There’s a trade to do here. The basic point to make is that gamblers don’t really care what form their risk takes. So investors who have both some returns and some risk should just give that risk to gamblers.

Imagine if Stake swapped their random number generator with another one partially based on the S&P 500. Every time you play roulette or Plinko or a slot machine on Stake, you get exposed to a tiny blip of what’s happening in the markets. For the individual player, it’s barely noticeable. But this lets Stake pass on risk from the markets. Stake can then turn up house edge per game by 10% per year since (a) that’s about the average return of S&P, and (b) measured every five seconds, this amounts to basically nothing and no one would notice. Then it goes out and buys a billion dollars worth of stocks.

Stake would be the most successful hedge fund in the world. At a 10% annual return and 0% risk, it beats out Citadel, Bridgewater, and Point72 on a risk-adjusted basis. It would be wildly far off the efficient frontier. And gamblers are no worse off for it!

Again, this should work. There are people in this economy who hate risk. There are people in this economy who love risk.

And again, this is not financial advice.

Alpha: 10% annual return, up to $2.5 billion if you own a crypto casino

Short Reselling

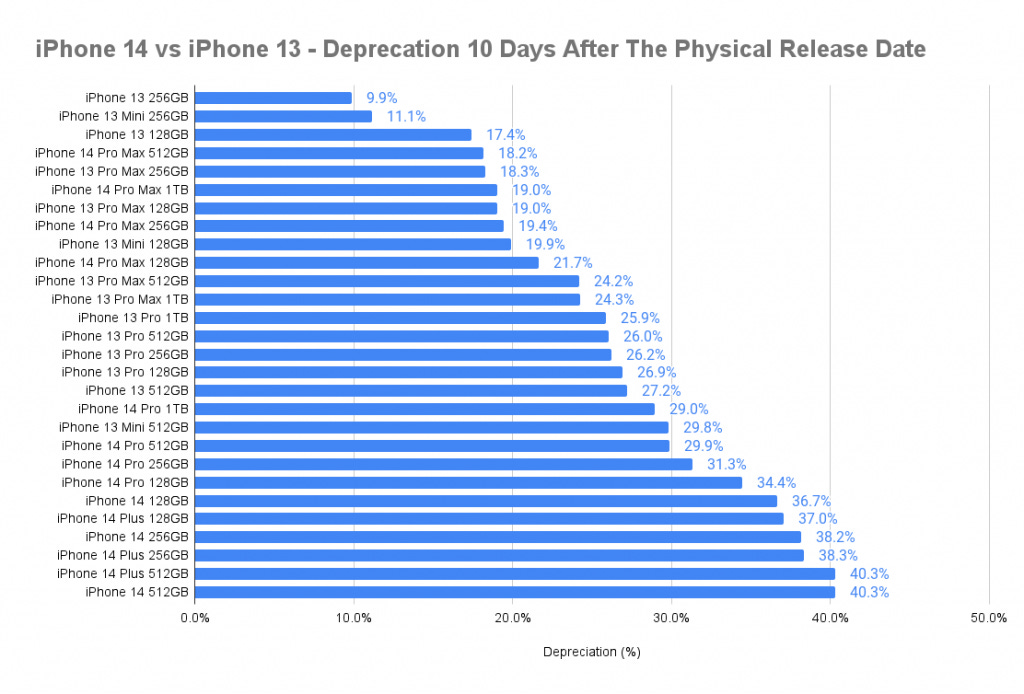

Depreciation. Most of us have the intuition that when a new model comes out, the old model becomes cheaper. It’s a predictable supply shock: a ton of people all of the sudden want to get rid of their old junk and will sell it for cheap. The pattern recurs for car redesigns, laptop upgrades, GPU improvements—you name it.

It happens for iPhones, a lot. After the iPhone 15 came out, the 14s lost “40% of their value within 10 days.” Forty percent! And it’s not even that big of an outlier. When a new iPhone gets released, a 15 to 30 percent drop in price is expected. Here are other models for comparison, compiled by SellCell, a phone retailer.

Something’s wrong here. For scale, even a 7% one-day decline in a price triggers a circuit breaker—a pause in trading—for the New York Stock Exchange. When prices move that fast, it means the market didn’t properly anticipate the price move before. Prices before the drop shouldn’t have been that high!

The problem, it turns out, is that same problem underlying the crazy meme stock

You can’t sell an asset you don’t already have, but what you can do is short an asset—borrow it from someone else for a fee and sell it on the spot, promising to give it back. When it’s difficult or expensive to execute a short, prices can remain inflated, which is why Gamestop still trades at nonsense prices. What we need is a way to borrow an iPhone 14, sell it before the iPhone 15 gets released, and then buy it back—good luck!

…or, you could be sneaky. Phone retailers like SellCell can get away with 10 business days worth of delivery delays. That’s ok for some people! Not everyone needs to get their phone immediately. These people enable a trade. If I were SellCell, I would undercut the market by 5% the days before the iPhone 15 release. I would sell as much as I could, offering a cheaper price for a slightly longer (15 days?) delivery. Then the 15 comes along, everyone’s clamoring to sell their cheap 14s, and I just redirect the flood to my previous customers!

If my math is right, you should be able to make a 20% return on each phone within a week, and the mere cost of one-day delivery. And perhaps your integrity. And certainly, your FINRA license.

Not. Financial. Advice.

Alpha: 20% return over 10 days for as many iPhones as you can package

Wish me luck! And if you’re inclined, share with anyone you know who doesn’t work for my employer.

For most of us, gambling winnings are taxed at a flat rate of 24%. That’s much bigger than the house edge, which is 1-10% for most games. This actually means that, if you’re an honest taxpayer, the very first bet you take in a calendar tax year loses 12% in expectation to the taxman. But this disappears once you have a position. If you currently have losses, then your gambling gains are untaxed. If you currently have gains, then your losses earn you tax write-offs. So if you ever discover a single-play any-denomination slot machine that pays 1% edge in your favor, you should only play if you already have a gambling balance.

You have to put in some effort here. If you repair appliances for a living, then courts have decided that gambling is not a business expense for you.

Single-zero roulette loses 2.7% to house edge. Your personal income tax rate is, say, 25%. For $4000 gambled, you lose $100 on average to the house. You win $500 from the IRS, from the half of the time that you get to offset taxes on your personal income. The risk of an audit is a rounding error—it’s something like 0.5%.

First, you can completely derisk this strategy by having a third friend bet on zero for a proportionate amount. Second, you’ll need to think through how to document the loss. One way to do this is through Player’s Cards. As of now, histories on Player’s Cards don’t get automatically reported to the IRS, but do give you credible receipts, if you chose to report. Third, scale it up!

See Merton (1972) and Ross (1978), or less obnoxiously, Investopedia on the efficient frontier and CAPM.

thoroughly enjoyed this read

Awesome read!